The Beginner's Guide To Normal Costing: A Comprehensive Explanation

What is normal costing?

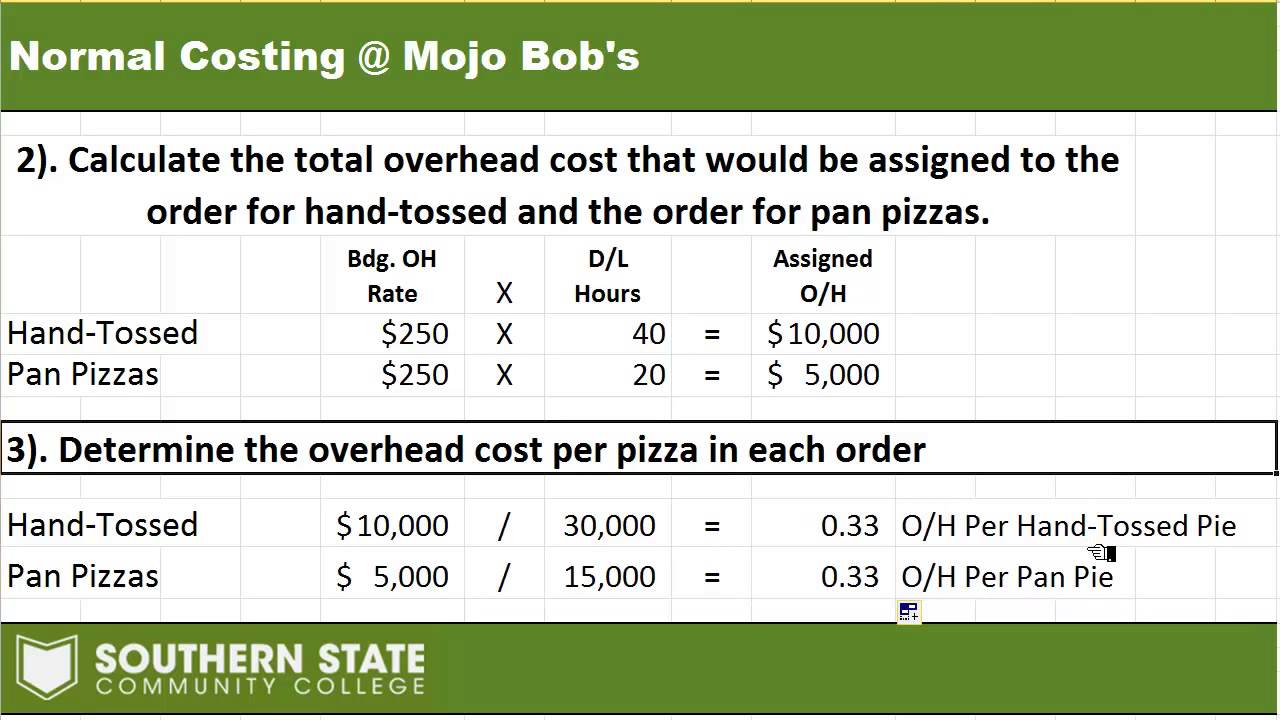

Normal costing is a costing system that allocates manufacturing overhead costs to products based on a predetermined overhead rate. This rate is calculated by dividing the total estimated manufacturing overhead costs for a period by the total estimated production for the same period.

The main benefit of normal costing over actual costing is that the costs of production are more stable and predictable. Because the predetermined overhead rate is based on estimates, it will not fluctuate as much as actual overhead costs. This can make it easier for businesses to plan and budget for their production costs. However, normal costing is not as accurate as actual costing because it does not take into account actual overhead costs.

Normal costing is still widely used by many businesses today. It is a relatively simple and straightforward costing system that can provide businesses with a reasonable estimate of their production costs. However, businesses should be aware of the limitations of normal costing and should consider using a more accurate costing system if necessary.

Topics covered in this article:

- Definition of normal costing

- Benefits of normal costing

- Limitations of normal costing

- Alternatives to normal costing

Normal Costing

Normal costing is a costing system that allocates manufacturing overhead costs to products based on a predetermined overhead rate. It is a relatively simple and straightforward costing system that can provide businesses with a reasonable estimate of their production costs. However, it is important to be aware of the limitations of normal costing and to consider using a more accurate costing system if necessary.

- Definition: Normal costing is a costing system that allocates manufacturing overhead costs to products based on a predetermined overhead rate.

- Benefits: Normal costing is a relatively simple and straightforward costing system that can provide businesses with a reasonable estimate of their production costs.

- Limitations: Normal costing is not as accurate as actual costing because it does not take into account actual overhead costs.

- Alternatives: There are a number of alternative costing systems available, such as actual costing and activity-based costing.

- Applications: Normal costing is used by a wide range of businesses, including manufacturers, retailers, and service providers.

The key aspects of normal costing are its simplicity, its ability to provide a reasonable estimate of production costs, and its limitations. Businesses should carefully consider the benefits and limitations of normal costing before deciding whether to use it.

Definition

Normal costing is a costing system that is used to allocate manufacturing overhead costs to products. It is based on the idea that overhead costs are incurred evenly throughout the production process, and that they can be assigned to products based on a predetermined overhead rate. The predetermined overhead rate is calculated by dividing the total estimated manufacturing overhead costs for a period by the total estimated production for the same period.

The definition of normal costing is important because it provides a framework for understanding how overhead costs are allocated to products. This information can be used to make decisions about pricing, production, and other business activities.

For example, a company that uses normal costing might use the predetermined overhead rate to calculate the cost of goods sold. This information can then be used to set prices for the company's products. Additionally, the predetermined overhead rate can be used to make decisions about production levels. For example, a company might decide to increase production if the predetermined overhead rate is low.

Normal costing is a relatively simple and straightforward costing system. However, it is important to be aware of its limitations. One limitation is that normal costing does not take into account actual overhead costs. This can lead to distortions in the cost of goods sold and other financial statements.

Despite its limitations, normal costing is still widely used by many businesses. It is a relatively simple and straightforward costing system that can provide businesses with a reasonable estimate of their production costs.

Benefits

The benefits of normal costing are directly tied to its simplicity and straightforwardness. Because normal costing is relatively easy to understand and implement, it can be a good option for businesses that are new to costing or that have limited resources. Additionally, normal costing can provide businesses with a reasonable estimate of their production costs, which can be helpful for planning and budgeting.

For example, a company that uses normal costing might use the predetermined overhead rate to calculate the cost of goods sold. This information can then be used to set prices for the company's products. Additionally, the predetermined overhead rate can be used to make decisions about production levels. For example, a company might decide to increase production if the predetermined overhead rate is low.

Overall, the benefits of normal costing include its simplicity, its ability to provide a reasonable estimate of production costs, and its usefulness for planning and budgeting.

Limitations

Normal costing is a costing system that allocates manufacturing overhead costs to products based on a predetermined overhead rate. This rate is calculated by dividing the total estimated manufacturing overhead costs for a period by the total estimated production for the same period. Because normal costing is based on estimates, it is not as accurate as actual costing, which takes into account actual overhead costs.

- Over-allocation or under-allocation of overhead costs: Normal costing can lead to over-allocation or under-allocation of overhead costs to products. This can occur when the actual overhead costs incurred during a period differ from the estimated overhead costs used to calculate the predetermined overhead rate. For example, if the actual overhead costs incurred during a period are higher than the estimated overhead costs, then the predetermined overhead rate will be too low. This will result in the over-allocation of overhead costs to products.

- Inaccurate product costing: The use of a predetermined overhead rate in normal costing can lead to inaccurate product costing. This is because the predetermined overhead rate does not reflect the actual overhead costs incurred to produce each product. As a result, some products may be costed at a higher or lower price than they should be.

- Difficulty in decision-making: The use of normal costing can make it difficult for businesses to make informed decisions about pricing, production, and other business activities. This is because the predetermined overhead rate does not provide businesses with an accurate picture of the actual overhead costs incurred.

Overall, the limitations of normal costing should be carefully considered before using this costing system. Businesses should be aware that normal costing is not as accurate as actual costing, and that it can lead to over-allocation or under-allocation of overhead costs to products. Additionally, normal costing can make it difficult for businesses to make informed decisions about pricing, production, and other business activities.

Alternatives

Normal costing is a widely used costing system, but it has certain limitations. As a result, there are a number of alternative costing systems that have been developed to address these limitations. Two of the most popular alternative costing systems are actual costing and activity-based costing.

- Actual costing: Actual costing is a costing system that assigns actual overhead costs to products. This is in contrast to normal costing, which uses a predetermined overhead rate to allocate overhead costs to products. Actual costing is more accurate than normal costing, but it is also more complex and time-consuming.

- Activity-based costing: Activity-based costing (ABC) is a costing system that assigns overhead costs to products based on the activities that are performed to produce them. This is in contrast to normal costing, which allocates overhead costs based on a single overhead rate. ABC is more accurate than normal costing, but it is also more complex and time-consuming.

The choice of which costing system to use depends on a number of factors, including the size and complexity of the business, the accuracy required, and the resources available. Normal costing is a good option for businesses that are small and have simple operations. Actual costing is a good option for businesses that require a high level of accuracy. ABC is a good option for businesses that have complex operations and require a high level of accuracy.

Applications

Normal costing is a costing system that allocates manufacturing overhead costs to products based on a predetermined overhead rate. It is a relatively simple and straightforward costing system that can provide businesses with a reasonable estimate of their production costs. As a result, normal costing is used by a wide range of businesses, including manufacturers, retailers, and service providers.

For manufacturers, normal costing is used to calculate the cost of goods manufactured. This information is then used to determine the cost of goods sold, which is a key component of the income statement. For retailers, normal costing is used to calculate the cost of goods sold. This information is then used to determine the gross profit, which is a key component of the income statement. For service providers, normal costing is used to calculate the cost of services provided. This information is then used to determine the gross profit, which is a key component of the income statement.

The use of normal costing by a wide range of businesses highlights its importance as a costing system. Normal costing provides businesses with a reasonable estimate of their production costs, which is essential for making informed decisions about pricing, production, and other business activities.

Normal Costing FAQs

This section provides answers to frequently asked questions (FAQs) about normal costing. These FAQs are designed to provide a better understanding of normal costing and its applications.

Question 1: What is normal costing?

Normal costing is a costing system that allocates manufacturing overhead costs to products based on a predetermined overhead rate. This rate is calculated by dividing the total estimated manufacturing overhead costs for a period by the total estimated production for the same period.

Question 2: What are the benefits of normal costing?

The benefits of normal costing include its simplicity, its ability to provide a reasonable estimate of production costs, and its usefulness for planning and budgeting.

Question 3: What are the limitations of normal costing?

The limitations of normal costing include its reliance on estimates, its potential for over- or under-allocation of overhead costs, and its inability to provide accurate product costing in all situations.

Question 4: What are the alternatives to normal costing?

The alternatives to normal costing include actual costing and activity-based costing. Actual costing is more accurate than normal costing, but it is also more complex and time-consuming. Activity-based costing is more accurate than normal costing and actual costing, but it is also more complex and time-consuming.

Question 5: Who uses normal costing?

Normal costing is used by a wide range of businesses, including manufacturers, retailers, and service providers.

Question 6: What are the key takeaways about normal costing?

The key takeaways about normal costing are that it is a simple and straightforward costing system that can provide businesses with a reasonable estimate of their production costs. However, it is important to be aware of the limitations of normal costing and to consider using a more accurate costing system if necessary.

Summary: Normal costing is a widely used costing system that can provide businesses with a reasonable estimate of their production costs. However, it is important to be aware of the limitations of normal costing and to consider using a more accurate costing system if necessary.

Transition: The next section of this article will discuss the applications of normal costing in more detail.

Conclusion

Normal costing is a costing system that allocates manufacturing overhead costs to products based on a predetermined overhead rate. It is a relatively simple and straightforward costing system that can provide businesses with a reasonable estimate of their production costs. However, it is important to be aware of the limitations of normal costing and to consider using a more accurate costing system if necessary.

The key takeaways about normal costing are that it is a simple and straightforward costing system that can provide businesses with a reasonable estimate of their production costs. However, it is important to be aware of the limitations of normal costing and to consider using a more accurate costing system if necessary.

Connect By Level: The Ultimate Guide To Mastering Tree Queries

Find Premium Prosciutto Near You

Explore The World Of Adjectives: Definition And Purpose

{kind=link}